INFORMATION PROVIDED BY THE GOVERNMENT OF CANADA

KEY POINTS

- Re-advanceable loans

- Access to additional funds without the use of lawyer

- Lender can change interest rate at any time (usually only when in default)

- Unsecured debt can be interconnected with mortgage (they can use your mortgage payment to pay off other debts if you miss a payment which puts you in default on your mortgage!)

- Mortgage is NON transferrable

- Highly impacts your renewal options

- Register mortgage for MORE than you borrow (up to 125%)

TYPES OF HOME EQUITY LINES OF CREDIT

There are two main types of home equity lines of credit: one that’s combined with a mortgage, and one that’s a stand-alone product.

HOME EQUITY LINE OF CREDIT COMBINED WITH A MORTGAGE

Most major financial institutions offer a home equity line of credit combined with a mortgage under their own brand name. It’s also sometimes called a readvanceable mortgage.

It combines a revolving home equity line of credit and a fixed term mortgage.

- You usually have no fixed repayment amounts for a home equity line of credit. Your lender will generally only require you to pay interest on the money you use.

- The fixed term mortgage will have an amortization period. You have to make regular payments on the mortgage principal and interest based on a schedule.

- The credit limit on a home equity line of credit combined with a mortgage can be a maximum of 65% of your home’s purchase price or market value.

- The amount of credit available in the home equity line of credit will go up to that credit limit as you pay down the principal on your mortgage.

Most major financial institutions offer a home equity line of credit combined with a mortgage under their own brand name.

As your equity increases, the amount you can borrow with your home equity line of credit also increases.

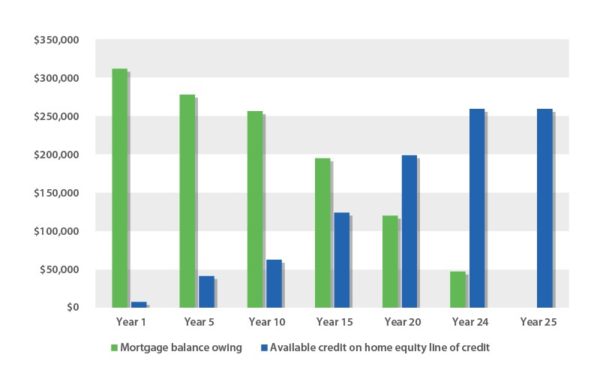

The following example is for illustration purposes only. Say you’ve purchased a home for $400,000 and made an $80,000 down payment. Your mortgage balance owing is $320,000. The credit limit of your home equity line of credit will be fixed at a maximum of 65% of the purchase price or $260,000.

This example assumes a 4% interest rate on your mortgage and a 25-year amortization period. Amounts are based on the end of each year.

Figure 1 shows that as you make regular mortgage payments and your mortgage balance goes down, the equity in your home increases. Equity is the part of your home that you’ve paid down through your down payment and regular payments of principal.

As your equity increases, the amount you can borrow with your home equity line of credit also increases.

Figure 1: Home equity line of credit combined with a mortgage

Figure 1 – Text version

You can see that your home equity line of credit didn’t increase in Year 25. This is because you had already reached the maximum credit limit for your home equity line of credit in Year 24.

Buying a home with a home equity line of credit combined with a mortgage

You can finance part of your home purchase with your home equity line of credit, and part with the fixed term mortgage. You can decide with your lender how to use these two portions to finance your home purchase.

You need a 20% down payment or 20% equity in your home. You’ll need a higher down payment or more equity if you want to finance your home with just a home equity line of credit. The portion of your home that you can finance with your home equity line of credit can’t be greater than 65% of its purchase price or market value. You can finance your home up to 80% of its purchase price or market value, but the remaining amount above 65% must be on a fixed term mortgage.

For example, you purchase a home for $400,000, make an $80,000 down payment and your mortgage balance owing is $320,000. The maximum you’d be allowed to finance with your home equity line of credit is $260,000 ($400,000 x 65%). The remaining $60,000 ($320,000 – $260,000) needs to be financed with a fixed term mortgage.

You’ll need a higher down payment or more equity if you want to finance your home with just a home equity line of credit.

You can also use your home equity line of credit to pay down debts you have with other lenders.

Creating sub-accounts in a home equity line of credit combined with a mortgage

A home equity line of credit combined with a mortgage can include other forms of credit and banking products under a single credit limit, such as:

- personal loans

- credit cards

- car loans

- business loans

You may be able to set up these loans and credit products as sub-accounts within your home equity line of credit combined with a mortgage. These different loans and credit products can have different interest rates and terms than your home equity line of credit.

You can also use your home equity line of credit to pay down debts you have with other lenders.

It’s important to be disciplined when using a home equity line of credit combined with a mortgage to avoid taking on more debt than you can afford to pay back.

STAND-ALONE HOME EQUITY LINE OF CREDIT

A stand-alone home equity line of credit is a revolving credit product guaranteed by your home. It’s not related to your mortgage.

The maximum credit limit on a stand-alone home equity line of credit:

- can go up to 65% of your home’s purchase price or market value

won’t increase as you pay down mortgage principal

You can apply for a stand-alone home equity line of credit with any lender that offers it.

You can apply for a stand-alone home equity line of credit with any lender that offers it.

A stand-alone home equity line of credit can be used as a substitute for a mortgage.

Substitute for a mortgage

A stand-alone home equity line of credit can be used as a substitute for a mortgage. You can use it instead of a mortgage to buy a home.

Buying a home with a home equity line of credit instead of a traditional mortgage means:

- you’re not required to pay off the principal and interest on a fixed payment schedule

- there’s a higher minimum down payment or more equity required (at least 35% of the purchase price or market value)

Using a home equity line of credit as a substitute for a mortgage can offer flexibility. You can choose how much principal you want to repay at any time. You can also pay off the entire balance any time without paying a prepayment penalty.

HOME EQUITY LOANS

A home equity loan is different from a home equity line of credit. With a home equity loan, you’re given a one-time lump sum payment. This can be up to 80% of your home’s value. You pay interest on the entire amount.

The loan isn’t revolving credit. You must repay fixed amounts on a fixed term and schedule. Your payments cover principal and interest.

QUALIFY FOR A HOME EQUITY LINE OF CREDIT

You only have to qualify and be approved for a home equity line of credit once. After you’re approved, you can access your home equity line of credit whenever you want.

You’ll need:

- a minimum down payment or equity of 20%, or

- a minimum down payment or equity of 35% if you want to use a stand-

- alone home equity line of credit as a substitute for a mortgage

Before approving you for a home equity line of credit, your lender will also require that you have:

- an acceptable credit score

- proof of sufficient and stable income

- an acceptable level of debt compared to your income

To qualify for a home equity line of credit at a bank, you will need to pass a “stress test”. You will need to prove you can afford payments at a qualifying interest rate which is typically higher than the actual rate in your contract.

Credit unions and other lenders that are not federally regulated may choose to use this stress test when you apply for a home equity line of credit. They are not required to do so.

The bank must use the higher interest rate of either:

- the Bank of Canada’s conventional five-year mortgage rate

- the interest rate you negotiate with your lender plus 2%

If you own your home and want to use the equity in your home to get a home equity line of credit, you’ll also be required to:

- provide proof you own your home

- supply your mortgage details, such as the current mortgage balance,

- term and amortization period

- have your lender assess your home’s value

You’ll need a lawyer (or notary in Québec) or a title service company to register your home as collateral. Ask your lender for more details.

You’ll need a lawyer (or notary in Québec) or a title service company to register your home as collateral.

TIPS BEFORE YOU GET A HOME EQUITY LINE OF CREDIT

- Determine whether you need extra credit to achieve your goals or could you build and use savings instead.

- If you decide you need credit, consider things like flexibility, fees, interest rates and terms and conditions.

- Make a clear plan of how you’ll use the money you borrow

- Create a realistic budget for your projects

- Determine the credit limit you need

- Shop around and negotiate with different lenders

- Create a repayment schedule and stick to it

QUESTIONS TO ASK LENDERS

- What do they require for you to qualify

- What’s the best interest rate they can offer you

- How much notice will you be given before an interest rate increase

- What fees apply

LEARN MORE ABOUT WHAT TO CONSIDER BEFORE BORROWING MONEY.

ADVANTAGES AND DISADVANTAGES OF A HOME EQUITY LINE OF CREDIT

Advantages of home equity lines of credit include:

- easy access to available credit

- often lower interest rates than other types of credit (especially unsecured loans and credit cards)

- you only pay interest on the amount you borrow

- you can pay back the money you borrow at any time without a prepayment penalty

- you can borrow as much as you want up to your available credit limit

it’s flexible and can be set up to fit your borrowing needs - you can consolidate your debts, often at a lower interest rate

Disadvantages of home equity lines of credit include:

- it requires discipline to pay it off because you’re usually only required to pay monthly interest

- large amounts of available credit can make it easier to spend higher amounts and carry debt for a long time

- to switch your mortgage to another lender you may have to pay off your full home equity line of credit and any credit products you have with it

- your lender can take possession of your home if you miss payments even after working with your lender on a repayment plan

These are some disadvantages of a home equity line of credit that are common to other loans:

- variable interest rates can change which could increase your monthly interest payments (your lender willprovide advance notice of any change)

- your lender can reduce your credit limit at any time (your lender will provide advance notice of any change)

- your lender has the right to demand that you pay the full amount at any time

- your credit score will decrease if you don’t make the minimum payments as required by your lender

Understand your home equity line of credit contract

Shop around with different lenders to find a home equity line of credit that suits your needs.

Each home equity line of credit contract may have different terms and conditions. Review these carefully. Ask your lender about anything you don’t understand.

INTEREST RATES

Home equity lines of credit can have different interest rates depending on how they’re set up.

They usually have a variable interest rate based on a lender’s prime interest rate. The lender’s prime interest rate is set by a financial institution as a starting rate for their variable loans, such as mortgages and lines of credit.

For example, a home equity line of credit can have an interest rate of prime plus one percent. If the lender’s prime interest rate is 2.85%, then your home equity line of credit would have an interest rate of 3.85% (2.85% + 1%).

You can try to negotiate interest rates with your lender.

They usually have a variable interest rate based on a lender’s prime interest rate.

Lenders will consider:

- your credit score

- income stability

- net worth

- your home’s price

- any existing relationship you may have with them

Tell them about any offers you’ve received from other lenders.

Your lender can change these rates at any time. Your lender must give you notice if there’s a change. Any change in the prime lending rate will affect your home equity line of credit’s interest rate and your payment amounts.

Make sure you only borrow money that you can pay back. This will help you manage a potential increase in interest rates.

LEARN ABOUT PROTECTING YOURSELF AGAINST RISING INTEREST RATES.

FEES

Fees may vary between home equity lines of credit.

Some common fees include:

- home appraisal or valuation fees: Your lender charges this fee to send someone to assess your home’s value

- legal fees: Your lawyer (or notary in Québec) or title service company charges this fee to register the collateral charge on your home

title search fees: This is another legal fee to ensure there are no liens on your home - administration fees: Your lender charges this fee for setting up and maintaining your account

- discharge or cancellation fees: Your lender or your notary (in Québec) charges this fee if you cancel your home equity line of credit and remove the collateral charge from the title of your home

Ask your lender about all the fees involved with your home equity line of credit.

MAKE A PLAN TO USE YOUR HOME EQUITY LINE OF CREDIT

Establish a clear plan for how you’ll use a home equity line of credit. Consider a repayment schedule that includes more than just minimum monthly interest. Make a realistic budget for any projects you may want to do.

You may be able to borrow up to 65% of your home’s purchase price or market value on a home equity line of credit. This doesn’t mean you have to borrow the entire amount. You may find it easier to manage your debt if you borrow less money.

They usually have a variable interest rate based on a lender’s prime interest rate.

If you borrow money to cover your monthly bills for an extended period of time...

DECIDE ON YOUR CREDIT LIMIT

You can negotiate the credit limit of your home equity line of credit. Lenders may approve you for a higher limit than you need. This can make it tempting to spend over your budget.

You can ask for a lower credit limit with your lender if it suits you better. This can keep you from borrowing more money than you need.

FIND OUT HOW TO CREATE AN EMERGENCY FUND.

CONSOLIDATING DEBT

You may consider using a home equity line of credit to consolidate high-interest debt, such as credit cards. A lower interest rate may help you manage your debt, but remember, it can’t solve the cause of your debt. You may need to take steps to address how you spend money.

A key step in paying off debt is to establish a payment plan. One way to do this is to convert a portion of your home equity line of credit into debt with fixed repayment amounts, much like a mortgage loan.

This way you can get into a habit of making regular payments. The interest rate and terms of the debt can be different from that of the home equity line of credit. Ask your lender for more information about this option.

Making a budget can also be a helpful way to manage debt. You can make adjustments to your spending as you pay off your debt.

USING HOME EQUITY LINES OF CREDIT TO INVEST

Some people borrow money from a home equity line of credit to put into investments. Before investing this way, determine if you can tolerate the amount of risk.

The risks could include a rise in interest rates on your home equity line of credit and a decline in your investments. This could put pressure on your ability to repay the money you borrowed.

GET MONEY FROM YOUR HOME EQUITY LINE OF CREDIT

Your lender may give you a card to access the money in your home equity line of credit. You can use this access card to make purchases, get cash from ATMs and do online banking. You may also be given cheques.

These access cards don’t work like a credit card. Interest is calculated daily on your home equity line of credit withdrawals and purchases.

Your lender may issue you a credit card as a sub-account of your home equity line of credit combined with a mortgage. These credit cards may have a higher interest rate than your home equity line of credit but a lower interest rate than most credit cards.

Ask your lender for more details about how you can access your home equity line of credit.

Your lender may give you a card to access the money in your home equity line of credit.

ou may be able to negotiate with a lender to cover some costs to transfer any credit products you may have.

TRANSFER YOUR HOME EQUITY LINE OF CREDIT

When your mortgage comes up for renewal, you may consider transferring your mortgage and home equity line of credit. You’ll likely have to pay legal, administrative, discharge and registration costs as part of the switch.

You may also be required to pay off all other forms of credit, such as credit cards, that may be included within a home equity line of credit combined with a mortgage.

You may be able to negotiate with a lender to cover some costs to transfer any credit products you may have. This can be difficult if you have different sub-accounts within your home equity line of credit combined with a mortgage that have different maturity dates.

Ask your lender what transfer fees apply.

CANCEL YOUR HOME EQUITY LINE OF CREDIT

You must pay off your home equity line of credit before you can cancel it. You can usually cancel within 10 days if you provide written notice.

Check your terms and conditions for more information about cancelling.